We believe everyone deserves a complete financial plan. A plan that incorporates your values, goals, and finances to help you lead a wealthy life now and build future wealth.

Our financial plans:

- define the current factors affecting your ability to build wealth,

- provide recommendations and a clear framework for tackling your concerns in living a wealthy life, and

- create an action plan for ongoing progress over our relationship.

Then, we continue to evaluate, implement, and monitor financial changes through ongoing progress meetings. We review major changes in your personal life, identify your priorities, and review progress toward building your wealth.

Our journey together is about being honest on where you want to go, where you are now, and making a best guess on how to bridge the gap. We help you balance the trade-offs in what you have to invest: money, time, energy, and skill.

We believe traditional Wall Street doesn’t fit Gen X & Y: the attention you receive should not be based on the amount of your investment assets.

Money decisions are often driven by desires to feel happy, safe and secure. By having a plan that matches your values with how you spend your money, you save time and increase happiness. Everyone deserves happiness!

Our fee structure is built on the complexity of your current financial situation – not based on your investment assets.

We believe each person and family is different: you should work with someone you can trust and who is an expert in your situation.

It is important to work with a financial advisor who understands your current situation. Do they have the professional network to assist you with your individual needs and do they understand your major concerns?

We focus on tech entrepreneurs and employees because we understand many of their particular issues:

Do you work for Amazon or Microsoft?

We understand their benefit plans and integrate RSU planning into our financial process.

We also know how to help you transition from the corporate life to a new adventure if this is your main goal.

Do you work for a local early startup?

If your startup does not have a 401(k) yet or provides limited health benefits, we can help you determine the best options for you.

Want more information on your stock options? We can help you think about the tax effects of these and make a plan for when to exercise your vested options.

Are you an early stage entrepreneur struggling with cash flow?

We can talk through budgeting, short term debt options, and how to think about your savings during this hard time.

As your career progresses, we assist you with tax planning for founder’s stock, minimizing risk in your portfolio, and protecting your family long-term.

Find out more about us on our About Us page.

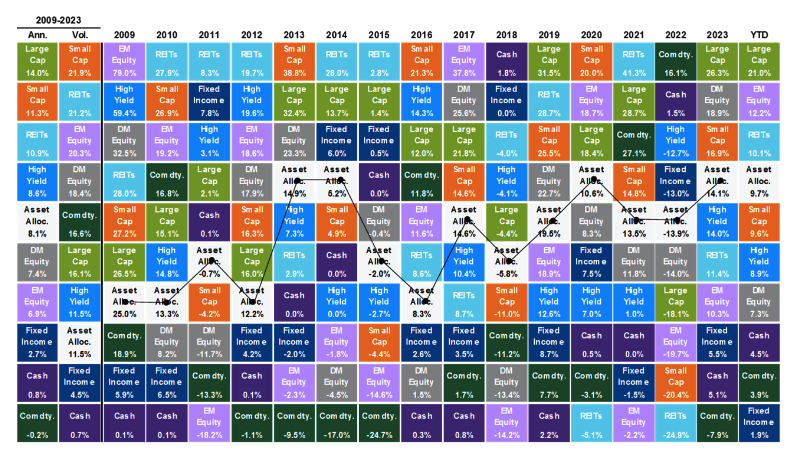

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024

JP Morgan returns from JP Morgan Quarterly Market Review, Q3 2024